Journal Entry For Equipment Purchase

Definition and caption

Purchases journal (also known equally purchases book and purchases day book) is a special journal used by businesses to record all credit purchases. All greenbacks purchases are recorded in another special journal known every bit cash payment periodical or cash disbursements journal.

When merchandise and their invoice are received from supplier, a responsible personnel from receiving department compares them with the re-create of the lodge placed by the purchase department. If quantity and quality of merchandise conform to the lodge, the merchandise are accepted and transferred to the warehouse. After it, an entry is immediately made in the purchases periodical on the basis of information obtained from the invoice provided by the seller.

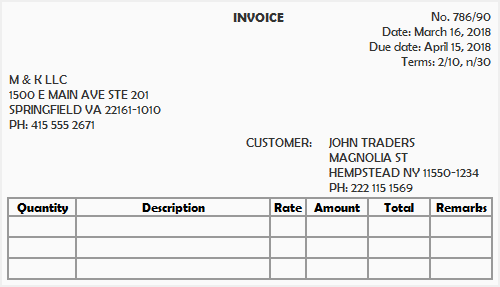

The invoice provided by the supplier (or seller) is known as the buy invoice or inward invoice. It normally provides the following information:

- The invoice number for the goods purchased.

- The engagement on which the invoice is prepared.

- The name, address, email, and phone number of both heir-apparent and seller.

- A proper description of trade i.e., quantity, quality, rates and full amount of the trade purchased.

- The details about terms and atmospheric condition of sale.

Format/specimen of purchase invoice

A simple purchase invoice with basic information may look like the following:

The bodily format or look of the invoice issued past a seller to his buyer may be slightly dissimilar from the above specimen but bones information provided therein is well-nigh similar.

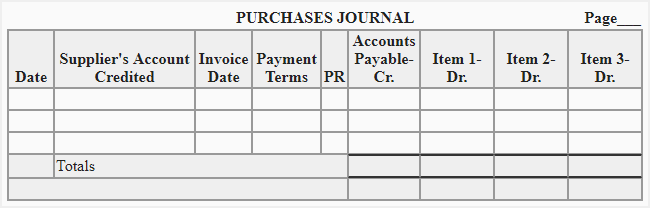

Format of purchases journal

The number of columns used in purchases journal depends on the needs of each business organisation. The commonly used format is given beneath:

Explanation of columns:

The entries in seven columns shown in to a higher place format of purchases journal are fabricated as follow:

- Engagement column: Date column is used to record the engagement on which the invoice belonging to appurtenances purchased is received.

- Supplier column: The supplier's proper noun is written in this column. Some businesses likewise include a brief description of goods purchased in this column.

- Invoice engagement column: The invoice date column is used to record the appointment on which the invoice is prepared by the supplier.

- Payment terms column: This column is used to record the payment terms allowed by the supplier.

- Reference column: At the end of each day, the entries from purchases periodical are posted to individual accounts in the accounts payable subsidiary ledger. If a computer software is used, these entries are immediately posted to subsidiary ledger. Reference column is used to record the account numbers of the accounts to which the entries have been transferred. If accounts are non numbered, the page number of accounts is recorded in this column.

- Accounts payable column: The amount payable on the invoice is recorded in this column.

- Items columns: These columns are used to enter the cost of individual items purchased from suppliers such as inventory, store supplies, part supplies and equipment etc. The number of item columns to be used on a purchases journal depends on the nature and requirement of each private business.

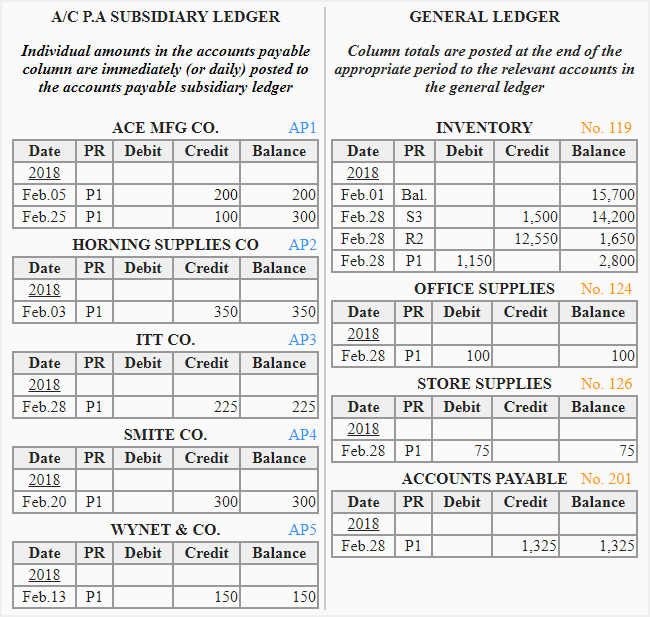

Posting the purchases journal to subsidiary and full general ledger

Posting to accounts payable subsidiary ledger:

At the finish of the day, each entry in the purchases journal is posted to the credit side of the relevant individual business relationship in the accounts payable subsidiary ledger.

Posting to general ledger:

At the end of the calendar month (or other appropriate catamenia), the column totals are posted to general ledger every bit follows:

- The total of accounts payable column is credited to accounts payable account in the full general ledger.

- The full of inventory column is posted to inventory business relationship in the general ledger.

- The total of all other items are posted to their relevant accounts in the general ledger.

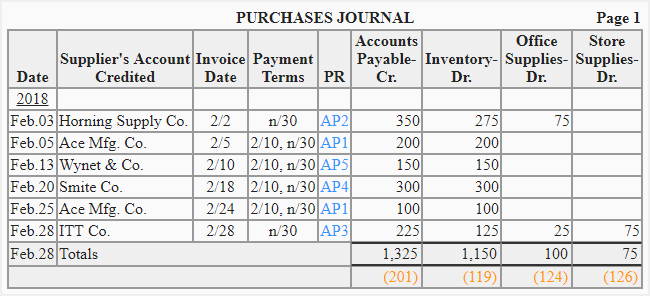

Consider the following example for a better understanding of the whole discussion.

Case

The post-obit example summarizes the procedure of entering transactions in the purchases journal and and then posting the entries to accounts payable subsidiary ledger and full general ledger accounts.

More from Special journals/subdivision of periodical (explanations):

Journal Entry For Equipment Purchase,

Source: https://www.accountingformanagement.org/purchases-journal/

Posted by: jenkinsexchilliked.blogspot.com

0 Response to "Journal Entry For Equipment Purchase"

Post a Comment